Air France-KLM’s plans to acquire a one-third stake in rival Virgin Atlantic cratered just two weeks after the deal passed muster with the U.S. Department of Transportation (DOT) on Nov. 21 — the final antitrust hurdle facing the proposed joint venture.

The airlines claimed the decision not to proceed was mutual, but Virgin majority owner Richard Branson said he didn’t want to dilute his investment after meeting some competitive goals through the recent deal for Flybe. The European Commission (EC) green-lighted the transaction in February.

An extended joint venture partnership among Virgin, Delta Air Lines and Air France-KLM will still go ahead.

Being left at the altar is not the worst outcome for the Franco-Dutch carrier, which recently announced a wide-ranging and expensive five-year plan. That plan calls for increasing profit margins to 7-8% in the medium term, restoring dividends and conducting a major fleet overhaul.

While Virgin’s joint venture with Delta helped the carrier compete with the British Airways-American Airlines alliance in recent years, network and flight connections have remained limited, precipitating the move to take on another partner.

To counter British Airways’ clout in Europe, establish a strong trans-Atlantic alliance and compete against low-cost carriers in that market, Virgin agreed in principle on the joint venture with Air France-KLM in May 2017. The deal called for Branson to reduce his stake in the carrier by selling a 31% interest to Air France-KLM for £220 million ($290 million), leaving him with a 20% holding in the carrier that he founded in 1984.

In a Dec. 2 letter to employees, Branson said, “Back in 2008, when British Airways tried effectively to merge with American Airlines, we fought the merger on behalf of our airline and our customers’ interests, with the ‘No Way BA/AA’ campaign on the side of our planes. Surviving against British Airways on its own was a struggle. But against the combined might of BA/AA, it would have been an impossibility. When competition authorities did somehow wave through the BA/AA partnership, we looked for a strong alliance of our own.

“To get the deal done, we initially thought our family would need to reduce its shareholding in Virgin Atlantic. I was willing to do so, reluctantly, to guarantee the long-term success of Virgin Atlantic,” he added.

Branson’s decision to walk away from the Air France-KLM deal follows the purchase of U.K.-based regional airline Flybe for the fire-sale price of £2.2 million by a Virgin Atlantic-led consortium earlier this year. Flybe will feed the long-haul networks of Virgin and joint venture partner Delta at Heathrow and Manchester airports. Virgin has been struggling to feed long-haul flights from U.K. cities other than London.The carrier is being rebranded as Virgin Connect. Virgin previously attempted to crack the U.K. domestic market with a carrier branded as Little Red but closed the operation in 2015.

Delta holds a 49% stake in Virgin, having agreed to acquire it in December 2012 from Singapore Airlines (SIA) for $360 million.

Branson used the letter to employees to take another shot at U.K. regulators, urging ministers to “shake up the status quo at Heathrow.” He has repeatedly taken aim at the domination of takeoff and landing slots at the European hub by International Consolidated Airlines Group (IAG), parent of British Airways. IAG holds over 55% of all Heathrow’s slots, with no other airline holding more than 5% of the remaining slots. Rules governing the allocation of new slots are being reviewed by the government. Virgin warns slots should be allocated in a way that enables development of a second flag carrier with the necessary scale to compete effectively with IAG.

Virgin has been active in entering joint ventures with other carriers. In October, China Eastern announced its intention to enter into a joint venture with Virgin, Air France and KLM, providing more options between Europe and China. The carriers in the joint venture stand to profit from trade with China as the world’s second-largest market for pharmaceuticals and the fastest-emerging market for the sector. And China has ambitions to become a powerhouse in exporting generic medication.

Only radical policy changes will encourage European fleet operators to invest in non-diesel trucks, according to Europe’s leading truck manufacturers.

Gerrit Marx, Chairman of the European Automobile Manufacturers’ Association (ACEA), said that binding sales quotas for manufacturers would do nothing to encourage transport companies to purchase alternatively powered trucks.

“If we are to convince hauliers to make the switch to low- and zero-emission vehicles on a large-scale, Europe urgently needs to introduce a strong package of consistent and predictable policy measures,” he said.

“Creating real market demand for low- and zero-emission vehicles should now be the priority.”

Reforms needed urgently

ACEA called for the rapid roll-out of dedicated charging and refueling infrastructure for trucks which it claims is “completely absent” at present.

The organization also said policy reforms should include “meaningful incentives to make these vehicles a commercially viable and competitive choice for transport operators, thereby fostering fleet renewal.”

And it argued that the revision of the Eurovignette Directive should allow “for the differentiation of road use charges by CO2 emissions.”

Emission reduction targets

The European Union (EU) adopted its first-ever CO2 standards for heavy-duty vehicles earlier this year. They state that manufacturers must cut carbon dioxide emissions from new trucks on average by 15% from 2025 and by 30% from 2030, compared with 2019 levels.

ACEA said the new CO2 targets would “oblige all manufacturers to focus on, and massively ramp up investments in, alternative powertrains.”

As well as chairing ACEA, Marx is also the president of CNH Industrial, which earlier this week launched a new range of electric and hydrogen trucks aimed at the European market. The trucks will be built by its subsidiary IVECO and powered by Arizona-based Nikola Motor Company.

The partners claim the new designs have the potential to reduce driver turnover rates.

An uphill haul in a diesel market

However, the latest fleet figures from ACEA illustrate the difficulty manufacturers such as IVECO will face when taking their new emissions-free models to market.

ACEA’s ‘Vehicles in Use – Europe 2019’ report found that at present 98.3% of all heavy- and medium- duty trucks above 3.5 tons on Europe’s roads run on diesel.

Electrically chargeable vehicles account for a negligible share of all trucks in circulation (0.01%, or one out of every 10,000 vehicles), while around 0.4% of all trucks in the EU run on natural gas.

“When we look at the total fleet of transport operators today, it is clear that the market will need to be completely turned around in an extremely short timeframe,” said Marx.

“In order to create a business environment where carbon-neutral solutions are the preferred option, all stakeholders will have to work together to transform the entire value chain of transport.”

According to ACEA’s new report, there are currently 6.6 million trucks on the EU’s roads. With more than 1.1 million trucks, Poland has the largest truck fleet in the EU, followed closely by Germany and Italy.

The report also found that the EU truck fleet is aging rapidly. Trucks are now on average 12.4 years old in the EU, compared to 11.7 years in 2013.

More FreightWaves and American Shipper articles by Mike

Rarely have container shipping lines played for such high stakes as they are right now. Not only are they attempting to pass on higher IMO 2020 low sulfur fuel bills, they are also in the final stages of agreeing to Asia-Europe annual contracts for next year.

Their success in negotiating both with shippers will go a long way toward deciding industry profitability next year, not least because Asia-Europe contract settlements will also set the stage for trans-Pacific liner-shipper contract negotiations in the second quarter of 2020.

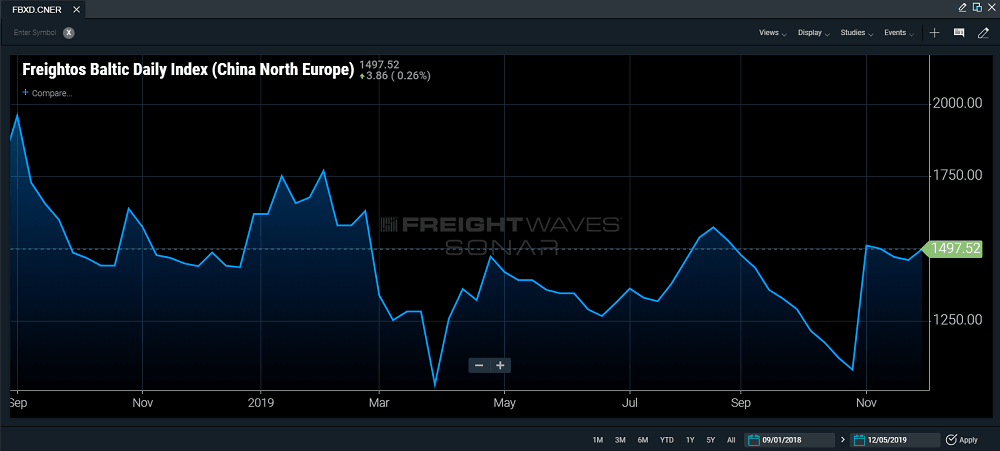

As previously detailed in FreightWaves, a key element of the strategy deployed by container lines has been to boost Asia-Europe spot freight rates to improve bargaining positions with shippers. This has proven a relative success in recent weeks (see the SONAR Freightos Baltic Daily China-North Europe Index below) , aided by the successful implementation of Nov. 1 General Rates Increases and the removal of capacity in the shape of multiple blanked sailings and scrubber retrofits.

Source: SONAR’s Freightos Baltic Daily Index (China-North Europe)

“They’re jacking up the short-term rates to try and get in a better position before locking in long-term rates,” explained Patrik Berglund, CEO of Xeneta, an Oslo-based ocean freight rate benchmarking and market analytics platform.

“The next three to four months will see massive volumes settling long-term rates before we move into the second quarter when trans-Pacific/U.S. volumes also will be settled,” Berglund said.

Capacity removal

Reducing slot supply has been the ‘go to’ tactic for lines looking to boost spot rates this year, so it was no surprise when Alphaliner reported earlier this week (Dec. 3) that the inactive container ship fleet had increased sharply across all main size segments to reach 225 ships capable of transporting 1.32 million twenty-foot equivalent units (TEU). As of Nov. 25, the ships accounted for 5.7% of the total fleet.

Shanghai-Rotterdam and Shanghai-Genoa spot rates are now 4% and 3% higher than a year earlier, respectively, according to Drewry. Even so, Berglund said European shippers were currently negotiating their rates from a position of strength compared to this time last year, not least due to the implementation of IMO 2020.

IMO 2020 is the game-changer

“IMO 2020 is the big thing on everyone’s lips,” he told FreightWaves TV’s ‘Port Report’ on Dec. 5.

“We see a major push to have floating bunker mechanisms inserted into long-term contracts for 2020 because of the uncertainty around IMO 2020 [fuel prices].”

He added, “But we’ve already seen some of the carriers have started to offer 12- and 24-month rates with no bunker fluctuations. That means two things to me. Either that they’re satisfied with current rate levels so they’re willing to take the risk. Or they’re concerned the rate level might drop so they’re trying to secure rates at current levels under contracts.”

Shippers should pay more?

Peter Sand, Chief Shipping analyst at BIMCO, said that while he expected freight rates would be decided by fundamental market balance, the entire cost of IMO 2020 fuels really should be passed on to end consumers of products shipped.

“But,” he added, “we have still to see the day when shippers care about lines’ profitability. Operators have worked hard to let shippers know that this is a cost to pass on. Time will soon tell whether that point have fully hit home.”

Sand also said, “No line can afford to shoulder the extra cost fully without sinking into loss-making territory.”

Back-haul leverage

Berglund expects supply and demand to be the deciding factor in the ‘who pays what’ debate over IMO 2020 costs. He thinks shippers with sizable back-haul Europe to Asia cargoes are particularly well-placed when negotiating bunker charges and contract prices with carriers.

“One of the biggest questions we have is how the front-/back-haul imbalance will make it difficult to spread any increased costs across carrier customer bases in a fair manner,” he said. “The ones on the back-haul, and particularly the ones with substantial volumes, have severe leverage when negotiating with the carriers and little incentive to split the bill with front haul shippers.”

Can lines hold firm on IMO 2020?

Neil Dekker, a senior analyst at Infospectrum, also identifies the mandatory use of low-sulfur IMO 2020 fuels for ships not fitted with abatement technology as a game changer for container markets next year. Nonetheless, he expects lines to hold a firm line on the imposition of IMO 2020 bunker surcharges.

“Lines that are not utilizing scrubbers will typically be paying higher prices for low sulfur fuel and will be looking to claim the costs back from shippers – this strategy is not new and liner operators have been preparing for it for some time,” he said.

Carriers do not have a strong track record when it comes to recovering costs for bunker price increases due to ‘all-in’ rate strategies. Historically, these strategies have made it more difficult for them to seek increased bunker fuel costs. However, Dekker expects this to change in 2020 due to the introduction of separate bunker surcharges.

“Lines are expected to take a hard line in enforcing these new bunker surcharges across all trade routes,” he added.

More FreightWaves and American Shipper articles by Mike

In a call this week, executives of freight forwarding giant DHL spoke on its observations of globalization based on DHL’s Global Connectedness Index (GCI) that monitors the flows of trade, capital, information and people across the world. John Pearson, the CEO of DHL Express, initiated the discussion by expressing globalization is “too big to fail” and that DHL’s primary motive was to connect people and improve lives through the expansion of trade that transcends borders.

Though globalization has taken a battering over the last two years due to protectionist policies, trade wars, and fragmentation of trade along regional lines, Pearson was confident that a global recession was still out of sight. That said, forecasts have continued to downgrade trade growth over the last few weeks of 2019 and a better part of 2020.

“For every trade war that seems to exist, there’s still multilateral and bilateral trade agreements being written,” Pearson said. “In fact, some of the purchasing managers indexes (PMI) are starting to rebound a little bit in some cases, depending on which country and which region you look at the forecast. And so far the IMF is forecasting some rebound, moderate or otherwise, to be witnessed in 2020.”

Steven Altman, a senior research scholar at the NYU Stern School of Business and the lead author of the DHL GCI, spoke at length on the causes and impact of global connectedness that had visibly declined over the last year. He pointed out that though the index did fall, it only reversed part of the increase that had propelled its figures to a record high in 2017 – noting that the index was still close to its all-time high.

The GCI is a good indicator of global connectedness health as it comprehensively measures how large international flows are relative to domestic activity (called depth) and how countries’ international flows are spread out globally around the world (called breadth).

Export depth measures countries’ exports against domestic consumption and export breadth looks at the spread of countries’ exports to markets all around the world – if most of their exports go to just a few destinations or are spread out. Altman explained that this helps the DCI to account for internationalized activity and to track if they are truly global.

Based on year-long data captured by DHL, it was apparent that capital investment shrunk in 2018, while trade, information and people flows had intensified compared to the year before.

Cross-border trade as a proportion of the world’s economic output is below its pre-crisis peak. Though trade had seen a rising trend in 2017 and extended that run in 2018 even during the onset of the U.S.-China trade war, the trend has died down over 2019, witnessing shrinkage. “Trade volume is still expected to continue growing, but trade growth is not likely to keep up with the GDP growth over 2020,” said Altman. “Current forecasts imply a decline in the trade part of the index back to around its 2016 level by 2020.”

Capital flows – which have remained the most volatile part of GCI – are also below the pre-crisis peak. However, there are reasons to believe in capital flow recuperation. While both foreign direct investment and portfolio equity investment declined in 2018, data from the first half of 2019 suggests some stabilization, though a robust recovery is still out of reach.

“According to data from the UN, the assets, sales and employment of multinational firms all grew in 2018. And there was also substantial growth in new green-field foreign investment and cross-border mergers and acquisitions. So while our capital flow measures were down last year, we do not see compelling evidence of a real retreat from corporate globalization,” said Altman.

Information flows have seen a significant surge, which Altman explained to be the part of the index that has seen the most growth since its initiation in 2001. However, the rate of growth has been lower since 2015, registering 1% expansion annually, against 4% growth from 2001 to 2014.

People flow continued to see growth across major indexes like tourism, international education and migration, with outbound tourism from emerging economies being the strongest driver of expanding flows of people across national borders.

Altman also touched on the trade flow shift from a more global outlook to being constricted along regional lines, which could alter the balance from long haul to short haul trade. “Our conclusion was that we do not see robust evidence, at least not yet, of a shift from globalization to regionalization. If trade were becoming more regionalized, we would expect the average distance across which countries trade to become shorter,” he said.

However, metrics that measure this shift show surprisingly different perspectives. Altman pointed out that this shift from long haul to short haul trade has been stable since 2012. “While there are shifts underway in geopolitics, economics and technology that could bring about a fracturing along regional lines, our analysis indicates that this remains just a possibility, rather than a historical fact,” said Altman.

The underlying operating model of airfreight is broken and needs fixing if customers are to receive the premium service they pay for. That was the stark message heard by air cargo stakeholders attending an executive summit hosted by TIACA (The International Air Cargo Association) in Budapest at the end of last month.

Kai Domscheit, CEO of CHI Deutschland Cargo Handling, a leading handler at Frankfurt Airport, spent time undercover “in old ripped jeans, a T-shirt and a cap, sitting next to the driver pretending I’m a trainee” secretly asking suppliers about their shipment and handling processes.

His conclusion was the airfreight industry “lacks integrity,” is “afraid of honesty” and could reduce international shipment lead times from around 6.3 days to 5.3 days if all parties were serious about improving service levels.

“When I question why we’re doing something in a particular way, it comes to the same thing: ‘Well, we’ve been doing this for the last 30, 40, 50 years,’” he said.

Domscheit was not alone in his criticism of air cargo logistics. Tan Siang Tang, CEO of Oman Air Sats, called for more cooperation across the supply chain. “At the moment we’re all operating in silos,” he added.

Johnny Voet, VP for air services at Liege Airport, said, “When you talk cargo, processes are not clear, not known or don’t exist, and there’s a lack of transparency and communication.”

“Dinosaurs” must leave their silos

Voet said shippers now expect track and trace and multimodal options and better supply chain predictability and punctuality and predicted that only those airfreight companies able to meet such expectations would prosper.

Domscheit called for radical change, telling airfreight stakeholders they must embrace digitalization and demand improvements in work processes.

He said operators and handlers must “do the right thing when no one is watching,” claiming many were “dinosaurs” afraid of “transparent communication because it might hurt the underlying business model.”

Domscheit told TIACA delegates to go back to their organizations, spend time undercover and in one week, “you will be extremely frustrated. … You’ll be shattered by the intel.”

He added, “At Frankfurt, trying to get cargo from air to landside takes six to 14 hours. The report will show 30 minutes to two hours. This is the magic trick, the disconnect.

“The reports I get are fudged, it’s not honest,” Domscheit said.

How to speed up airfreight

Air cargo analysts contacted by FreightWaves in the aftermath of TIACA’s executive summit took a more nuanced view on how and where the airfreight sector can improve its operating model.

FreightWaves’ in-house air cargo market expert Jesse Cohen believes that speeding up air cargo shipment times is usually a matter of addressing issues on the ground, especially when it comes to trying to compete for cargo against integrators.

“Airplanes basically fly the same speed, so the difference for forwarders competing with integrators is getting their arms around the ground components and the timely information flows between multiple parties on the ground surrounding that,” he said.

“Today we are seeing greater adoption of technology solutions, business processes and data sharing by airport cargo stakeholders in various locations in Europe and North America.

“These show a lot of promise toward driving efficiency and eliminating wasted time in processing a shipment,” Cohen said.

Putting shippers first

Brandon Fried, executive director at the Airforwarders Association (AfA), believes that while speed is air cargo’s primary value proposition, meeting customer expectations is not only about transit times.

“This is why most forwarders offer a wide range of transportation options helping shippers select the right service for the budget and commitment at hand,” he said.

“For example, we all know that, generally, next-day delivery is more costly than more economical deferred transit. Speed is only one part of a more complex equation because shipper demands vary.

“Also, regulatory requirements at the origin, transshipment points and destination can often impact transit time, varying widely depending upon the countries involved,” Fried said.

Learn from the integrators

Cathy Morrow Roberson, founder and head analyst at Logistics Trends & Insights, said airfreight could be speeded up if carriers worked better with supply chain partners — airports, shippers and road/rail transportation providers.

“The right service offerings, such as those the integrators offer, are another thing to consider. What does the final customer need?” she added.

“Provide options — not all customers will require same-day/next-day delivery,” Roberson said. “Understand customer needs.

“And, of course, price such services appropriately so that shippers and the carriers themselves benefit,” she continued.

“But first you’ll need to get all the players to cooperate.”

More FreightWaves and American Shipper articles by Mike

Officials at East Midlands Airport (EMA), which is second only to London Heathrow in terms of annual cargo volume among U.K. airports, announced that preliminary talks are ongoing with counterparts at Chongqing Jiangbei International Airport in southwest China and Sichuan Province officials aimed at starting direct cargo flights between the two airports.

EMA has not yet pitched carriers to start China service, spokesman Ioan Reed-Aspley said.

The airport is the U.K.’s largest dedicated air cargo operation, handling 368,000 tons of freight yearly valued at £11 billion ($14.5 billion), of which involves movements between non-European countries. The airport plans to triple freight volume to 1 million tons annually within the next 10 to 20 years. Chongqing Airport has capacity for 1.1 million tons of cargo.

EMA is expanding cargo capacity, adding apron space for freighter aircraft as it prepares for increased volumes driven by e-commerce. EMA officials also cite the airport’s location in Leicestershire, adjacent to major road networks, as an advantage for getting goods in — and out — of U.K. and European markets.

Major logistics specialists, including DHL, UPS, FedEx/TNT and U.K. Royal Mail, have operations at the airport. In 2020, further cargo growth at EMA is expected when UPS opens a new £114 million facility that will double the integrator’s capacity. EMA is the U.K. cargo hub for UPS. Online retail giant Amazon, which has a fulfillment center near EMA, operates several daily flights. Cargo carriers, including ASL Airlines, Cargolux, Etihad Cargo and Qatar Air Cargo, operate into EMA.

EMA recorded its highest-ever monthly cargo volume in October, despite a downturn in the overall airfreight market this year. Approximately 35,000 tons passed through the airport, eclipsing the previous record set in November 2018, when cargo operators handled slightly over 34,000 tons.

Sichuan is one of the largest Chinese provinces, with a population of 81 million people, 15 million more than the whole of the U.K. It is an economic corridor that connects the hinterland of southwestern China to south and central Asia. Sichuan Province has the largest consumer market in western China, providing export opportunities for U.K. and European shippers.

Airport officials point to the success of Manchester Airport, some 80 miles from EMA, as an indicator of potential cargo throughput that could emanate from a dedicated China service. Manchester is the third-busiest airport in the U.K., after Heathrow and London Gatwick. EMA and Manchester Airport share the same owner in Manchester Airport Holdings, the U.K.’s largest airport owner.

In the two years following the launch of service between Manchester and Beijing, the value of exports on the route grew 41% to £1.29 billion. The value of combined exports and imports from the northwest of England to China is now 7% higher than it was before direct flights were launched from Manchester (2018 vs. 2015).

Manchester’s cargo operation is small in comparison to EMA’s operation. Manchester offers direct passenger flights to China but no dedicated freighter service. Exported goods from Manchester to China, which have been responsible for the largest year-on-year volume growth, include food and textiles.

Of the several pain points faced by truckers across Europe, safe truck parking has remained a ubiquitous issue that drivers constantly grapple with – reflected by a European Commission (EC) study, which points to unsafe parking spaces as the hotspot for cargo theft that exceeds € 8.2 billion annually. Road freight accounts for roughly 50% of all tonne-kilometers in Europe, making it the primary mover of the economy and helping garner the attention of the European Union (EU) over the truck parking issue.

In its study earlier this year, the EC vowed to establish a denser network of safe and secure truck parking areas (SSTPAs) and initiated the creation of a standard that can clearly outline security levels that would be needed to tackle the issue of cargo theft. This standard would be common across the industry, stipulate guidelines that ensure reliability, and provide comprehensive maps that provide the locations of SSTPAs in Europe.

The Transported Asset Protection Association (TAPA) for the Europe, Middle East, and Africa (EMEA) region has announced its strong support for “all initiatives, standards and regulatory requirements” from the EC to address the safety and security of truckers and cargo, while also pushing for collaboration with its existing industry standard on safe truck parking.

The Parking Security Requirements (PSR) is an industry standard that TAPA developed a year ago, which includes a tiered certification program for parking place operators (PPOs) helping foster an increase in the number of secure parking spots within Europe. TAPA’s ever-expanding database currently accounts for around 5,000 safe truck parking spaces spread across 10 countries in the EMEA region.

“We believe that the EU must work with the industry while creating its standard, as it’s for the industry, from the industry, and at the end of the day, paid for by the industry,” said Thorsten Neumann, the president and CEO of TAPA. “This is the reason why we say that if the EU is looking to create a standard on secure parking places, they need to accept existing standards.”

The TAPA asks for mutual recognition, as there have been instances in the past where standards created within the industry in silos failed to get wider adoption. However, TAPA’s PSR standard has found significant traction, with the stakeholders buying into its regulations and creating a tangible change within the industry.

“At TAPA, we want to actively contribute and provide our expertise to the EU. It is important that the industry does everything possible to mitigate risks, while the EU and its politicians create the right awareness and mindset change to make that happen,” said Neumann.

To develop its PSR standards, TAPA invited all the key stakeholders to the table with a goal to connect every segment of the supply chain – including shippers, freight forwarders, trucking businesses and insurance companies. Neumann explained that it is critical for supply chains at-large to understand where the risk was coming from, as risks are rarely stagnant and evolve over the years.

“Our biggest hope is that the EU accepts our industry standard from a mutual recognition point of view and links it to their own standard. From their press release, it is clear that they are looking at getting 20 certifications by 2020, while we have already reached that,” said Neumann. “Our goal now is to have 80 certifications, and so it is a no brainer that if the EU accepts our standard, they can double or even quadruple their own numbers.”

Customers of retailer Argos, which operates in the U.K. and Ireland, could face disappointment during the Christmas season after staff at one of the retailer’s distribution centers voted to strike in a long-running row over pay.

Argos is a major player in the retail sector with more than 883 retail shops, 29 million shop customers yearly and nearly 1 billion online visitors annually.

Yard and highway drivers employed by UPS at Argos’ flagship distribution center at Barton in Staffordshire, England, have scheduled a 15-day strike following a 10-month wage dispute, according to a Dec. 3 announcement from trade union Unite.

Unite said that 90% of union members at the site voted in favor of the strike action, which will start late on Dec. 17 and continue through the end of the year.

The union warned that without the on-site and over-the-road drivers to maneuver loads on and off the distribution center, work will effectively grind to a halt, causing severe disruption to Argos at its busiest time of the year.

UPS has pledged to put contingency plans in place to minimize disruption, but is hopeful the job action can be averted.

The Barton site is a critical hub in Argos’ national network and the location from which all high-end electrical items, including smartphones, laptops and televisions, are shipped to regional Argos distribution centers for delivery to stores.

“Unite has been waiting for an offer in response to our members’ pay claim since March. Drivers and shunters have been treated with contempt and have had enough,” Rick Coyle, the union’s regional officer, said in a statement.

“Our members only received an offer of a voucher scheme that was so devoid of details that it could not be put to a ballot. Our members do not want to cause disruption for Argos’ customers over the Christmas period, but they have been left with no choice but to strike.

“It is now up to UPS to ensure this dispute does not extend right across the busiest time of the year for Argos by tabling a sensible offer that our members can actually vote on,” Coyle said.

Separately, Unite called on logistics company Supply Chain Coordination Ltd. (SCCL), which supports Unipart and National Health Service (NHS) supply company, to take part in talks mediated by arbitration service Acas over pay for truck drivers earning an industry low £10.24 ($13.42) per hour.

The drivers, who are employed nationwide by Unipart and drive HGV and 7.5-ton vehicles, deliver general equipment and supplies to NHS, which is wholly owned by the U.K. secretary of state for health and social care.

SCCL has been mandated to save the NHS £2.4 billion by 2022-23 by unifying health service procurement. Unite has warned, however, that this “must not result in a race to the bottom for drivers’ pay and conditions.” Drivers are seeking a pay increase in line with inflation as well as full sick pay benefits.

Talks between Unite, Unipart and SCCL broke down in late November, despite a deal close to being reached. Unite urged Unipart and SCCL to commit to negotiations mediated by Acas, stressing that it would far rather resolve the dispute than ballot members for industrial action.

Swiss WorldCargo, the freight division of Swiss International Air Lines, opened its Cancun, Mexico, export-handling station Dec. 2. This service expansion allows all flights between Zurich and Cancun to carry cargo on both inbound and outbound legs.

Swiss WorldCargo connects Cancun and Zurich with a thrice-weekly A340-300 service, operated by Edelweiss, a sister company of Swiss International Air Lines. The aircraft will offer a payload in excess of 15 tons on each leg of the flight.

In Cancun, Skylog, a member of the ECS Group, will act as sales agent with shippers, while Swissport will oversee ground operations. Inbound flights depart Zurich in the afternoon and arrive in Cancun in the evening, while outbound flights leave Cancun in the evening and arrive in Zurich the following afternoon.

With this schedule, customers in Mexico benefit from late delivery times in Cancun as well as convenient arrival times in Zurich for many same-day connections to Swiss WorldCargo’s destinations in Europe, Africa and Asia.

“With this new development, we will create additional export options for numerous customers shipping a wide variety of products from the Yucatan Peninsula to Switzerland, Europe and the rest of the world. Having a strong foothold in the Latin American market remains a critical focus point for us,” said Hendrik Falk, head of cargo for the western region of the U.S., South and Latin America, in a news release.

What would happen to global trade if the European Union (EU) implemented some form of carbon pricing for ocean shipping and the International Maritime Organization (IMO) did not follow suit, or did so years later, leading to a permanent or temporary ‘Balkanization’ of carbon-emission regimes?

On Dec. 2, the new president of the European Commission, Usula von der Leyen, affirmed during a speech at the United Nations climate conference (COP25), “Ten days from now, the European Commission will present the European Green Deal.” She said that in March 2020, “we will propose the first-ever European Climate Law, [which] … will include extending emission trading to all relevant sectors … [including] transport.”

EC President Usula von der Leyen. Photo courtesy of Shutterstock

The possibility of unilateral carbon pricing was cited in the International Monetary Fund working paper, “Carbon Taxation for International Maritime Fuels: Assessing the Options,” published in September 2018. That paper pointed out that “the European Parliament has declared its intention to proceed with regional carbon pricing in the absence of a global agreement.”

On one hand, recent developments in the EU, the perennial sluggishness of IMO progress and the inherent hurdles to global consensus suggest that a “EU now, IMO later” scenario is conceivable.

On the other hand, that would only be possible if EU member states unanimously agreed — which is an enormous “if.”

Challenges to a global solution

The difficulty in obtaining global approval of a carbon tax or some other carbon-pricing system for marine emissions was highlighted by recent events at the IMO. During of the IMO’s Intersessional Working Group on Reduction of Greenhouse Gas (GHG) Emissions from Ships that concluded on Nov. 15, a proposal to limit ship speed to reduce carbon emissions was set aside in favor of target-based measures.

Numerous shipowners backed the slow-steaming proposal. That’s not surprising. Speed limits would significantly reduce their fleets’ GHG emissions while virtually guaranteeing that the cost of those reductions would be paid by charterers and cargo shippers. Slower speed reduces effective vessel supply and increases freight rates.

Prior to the IMO working group meeting, Ridgebury Tankers CEO Bob Burke predicted the negative outcome of the slow-steaming proposal while speaking on a panel at the Marine Money conference in New York on Nov. 13.

Ridgebury Tankers CEO Bob Burke. Photo courtesy of John Galayda/Marine Money

“Speed limits would cost the charterers money, meaning there will be a lot of pushback from them — I doubt there will be any traction, ” he said.

“When OPA ’90 [the law stemming from the Exxon Valdez spill] was being discussed, hydrostatic loading would have solved the problem immediately [versus the chosen transition to double hulls].” In hydrostatic loading, the cargo level is limited to assure that if the tank is breached, seawater flows in and oil doesn’t flow out. “That was categorically rejected by the oil companies because it would cost them money,” noted Burke.

That same pushback seems plausible if a global carbon pricing system is pursued. The IMF paper made the case for an international carbon tax. During the meeting of the Global Maritime Forum in late October, BW Group chairman Andreas Sohmen-Pao said, “To meet international shipping’s decarbonization challenge, the maritime industry needs a carbon levy. It is coming and we should shape it.”

During the Marine Money forum, DryShips CEO George Economou was asked about the prospects for a global carbon tax on shipping. He replied, “The problem is we can talk about it, but it’s the oil companies that will take the decision.

DryShips CEO George Economou. Photo courtesy of John Galayda/Marine Money

“Can you imagine if the oil companies said they would put aside 30% of their profit to develop something new [i.e., fund the development of low-carbon-emitting shipping solutions]? If you were an investor in an oil company would you like that? No. So I think they will resist it, and it’s not going to happen anytime soon.”

It is not just the oil companies. Most of the world’s largest corporate entities depend upon the cheap movement of goods across the oceans. In some cases, these entities are state-owned.

A country’s leadership could balk at implementing carbon levies on shipping if the added price jeopardized its imports, exports and economic growth. That creates a high hurdle to global consensus.

Challenges to a regional solution

The challenges to a non-global solution, such as an EU-only carbon-pricing system, were addressed in the World Bank working paper, “Regional Carbon Pricing for International Transport,” published in January 2018.

That paper noted that a regional levy would have to be implemented by the port state (not a flag state, i.e., the ship register) and would have to incorporate GHG emissions beyond the port state’s territorial waters. “The scope of port-state jurisdiction with regard to activities that take place beyond the state’s territorial waters is a debated issue,” said the paper.

Assuming the EU or any other regional body could win the legal jurisdictional argument, the next challenge is preventing shipping interests from gaming the system. If the carbon pricing applies to the time at sea between the arrival of the cargo and its departure from the previous port, shippers could increase the use of transshipment at a nearby hub to minimize the transport covered by the carbon pricing.

Another complication arises with exports of petroleum products and liquefied gas. Such cargoes are often traded multiple times while in transit. The final destination is often not known when the ship departs. If the EU had a carbon-pricing system, how would it determine the pricing for such a destination-flexible cargo, or prevent that cargo from being “sold” to an entity in a nearby port and then ultimately resold farther afield?

What the World Bank working paper does not address is the even greater obstacle to regional carbon pricing arising from basic shipping-market dynamics. If costs are passed along to cargo shippers, it would impact the price of EU imports and the competitiveness of EU exports versus other regions. If costs are borne by vessel interests, those vessel interests — which can sail anywhere in the world — would have less incentive to serve EU ports, meaning that costs would still ultimately be borne by EU importers and exporters due to scarcer vessel supply.

Political challenges to an EU-only solution

The whole question of whether an EU carbon regime for shipping could exist in the absence of a global regime may be based on the flawed premise. According to Pablo Rodas-Martini, senior associate of SQ Consult, a Dutch company specializing in climate change and carbon markets, “The possibility of a carbon tax imposed by the European Commission is very low — it’s almost impossible.”

Rodas-Martini told FreightWaves, “The reason is straightforward: According to the regulations of the EU, any new tax must be agreed by unanimity by all member states. Such a requirement makes it almost impossible to think that a carbon tax will be proposed for the shipping sector.

“The approval of the energy tax took about 12 years due to this requirement. In the leaked text on the green deal, it is mentioned that the new commission wants to ‘pursue efforts’ to scrap this unanimity rule but, well, we are still very far from that point.

“More than a carbon tax to the shipping industry, the European Commission and the European Parliament have mentioned in the past that shipping should also be included in the European Union Emission Trading System [EU ETS], in a similar way as the aviation sector was added a few years ago,” he continued.

“That EU ETS includes power plants and energy-intensive industries across the EU. However, in the case of aviation, only the intra-European flights have been added to the EU ETS. If shipping is added, it would be under similar conditions: only the intra-European cargo, which would leave most of the shipping operations outside the EU ETS, since in the case of shipping, the intra-European share is much lower than the intra-European share for the aviation sector.

“This issue — the relatively small share of intra-European cargo for shipping — will force the EU to put more pressure on the IMO, [to push the] IMO to implement a much more ambitious climate change strategy,” he concluded.

To date, confusion over the IMO’s future course on carbon emissions has actually been a positive for shipowners’ profit prospects. Uncertainty has spurred fears about the obsolescence risk of newbuildings. This concern has drastically reduced new ship contracting, which limits future vessel supply and supports freight rates.

Eagle Bulk CEO Gary Vogel. Photo courtesy of John Galayda/Marine Money

The industry is well aware that carbon-related consequences could turn negative. As a result, it is seeking to proactively address the issue through the Global Maritime Forum and via voluntary industry initiatives such as Getting to Zero Coalition and, on the ship-finance front, the Poseidon Principles.

As Eagle Bulk (NASDAQ: EGLE) CEO Gary Vogel explained at the Marine Money forum, “If you look back at ballast-water treatment and to some extent IMO 2020, we’ve hopefully learned that it’s very important to have a seat at the table. Particularly with ballast-water treatment, with all the misinformation and the starts and stops – that’s not helpful.

“If you look at decarbonization and how much bigger that is for the industry, whether it involves a carbon tax or other means, we know that we have to have a better outcome [than occurred with previous regulatory initiatives]. It’s about being there, having a voice at the table and making sure that we are on a better trajectory, because this is too big of an issue to bolt the wings on while we’re in mid-flight.” More FreightWaves/American Shipper articles by Greg Miller