The onset of the new decade will usher in the International Maritime Organization’s (IMO) sulfur cap regulations to the maritime industry, spurring the global push to make transportation more sustainable and carbon-efficient. Within Europe, much has happened in terms of regulations and policymaking that look to steer a modal shift towards rail from hauling freight over road.

The “European Green Deal” is a landmark action plan unveiled by Ursula von der Leyen, the president of the European Commission (EC), to address greenhouse gas emissions (GHG). The goal of the European Green Deal is to achieve climate neutrality by reducing GHG to a minimum and offsetting all remaining emissions through climate protection measures.

In an EC meeting on Dec. 11, von der Leyen explained that the European Green Deal was about fostering a growth strategy that “gives back more than it takes away.” The deal offers a roadmap that encourages efficient use of resources, creating a circular economy that reduces biodiversity loss and decreases emissions.

In the context of the transportation industry, the deal prioritizes a 75% shift of EU freight traffic from road to rail and reduces GHG emissions by 90% by 2050. The European Parliament has advocated for a drastic increase in mid-term targets, pushing for a 55% reduction in overall GHG emissions (from 1990 GHG levels) by 2030 from the current 40% target for the same year.

Transportation’s share of Europe’s total emissions stands at 24% today, which if contained, could prove to be a massive impetus towards the EC’s vision of a sustainable tomorrow.

In the context of European rail transport, the segment already has a great deal in its favour. For instance, the railways do spectacularly well covering their variable costs and externalities like emissions, air and noise pollution through added charges based on distance travelled. Studies conducted by the EC suggests that rail transport’s externalities are small in comparison with other modalities, both for passenger and freight movement.

European railways also have a higher degree of electrification compared to other developed economies, making vast sections of rail lines environmentally sustainable. Four out of every five trains in Europe run on electricity, with the sector already going beyond the intended renewable energy target that the EU set for the transport industry by 2030.

However, a freight movement shift towards rail would require significant infrastructure investment because at this time, European railway systems are focused more on moving people than freight. The differences are glaring when the systems are compared to the American rail industry, which over the years has undergone structural changes that have enabled longer trains and heavier axle loads on their railroads.

The length of an average U.S. freight train is around 2,000 meters, with the longer ones exceeding 6,000 meters in length. In Europe, the length of trains is restricted to 750 meters – a diminutive length compared to U.S. trains. This is primarily due to a difference in perspective; the European rail system is fine-tuned towards moving people rather than freight. Longer trains are undesirable as it would be harder for trains to brake rapidly – a necessity for trains transporting people.

European rail also contends with restrictions on vertical height, which reduces the load that can be carried in a single rail car. Newly built rail cars in the U.S. top 7 meters from the rail – a full 30% higher than an average European rail car. Increasing the vertical height of cars would require Europe to invest in re-engineering height clearances across tunnels and also in bolstering rail lines, as they would have to take up heavier axle loads as railcars get bigger.

The European Green Deal could be a starting point for Europe’s transition from road to rail freight, but it is essential to look at the challenges that lie in front of the industry. Reforms from the EC would have to be followed up with strategic investment in the sector, which if materialized, can lead to a significant reduction in emissions across the transport sector.

DP World’s (NDAQ DXB: DPW) recent announcement that it indirectly acquired a 77% stake in Asian ocean shipping feeder and short-sea carrier, Feedertech, has further advanced the container terminal operator’s goal of becoming an end-to-end logistics provider.

The deal, which is due to close at the end of the year, will see Europe-focused and Denmark-headquartered Unifeeder (which is owned by DP World) buy just over three-quarters of Asia-focused and Singapore-based Feedertech. The balance of Feedertech will remain in the hands of the company’s founder, Ali Maghami.

Meanwhile, Unifeeder is, as its name implies, also a feeder operator and short-sea carrier.

A “feeder” carrier is a sea-going carrier that typically hauls containers from smaller, regional seaports, to much bigger ports for later pick up by larger container ships. Feeders usually sail the ‘spoke’ in a hub-and-spoke model of cargo trans-shipment.

Meanwhile, the definition of “short sea” varies widely but it is usually equivalent to something like “coasting” or “coastwise” trade and it normally means marine freight carriage without necessarily involving a large hub port or the crossing of a large sea or ocean.

A foothold in the intra-Asia markets

Commenting on the benefit to Europe-focused Unifeeder of buying an intra-Asia specialist, Daniel Richards, a senior analyst with consultancy Maritime Strategies International (MSI), told FreightWaves: “The Feedertech acquisition gives Unifeeder – and by extension, DP World – a foothold in the intra-Asia markets, which are expected to be one of the more dynamic containership markets in the years ahead. It seems DP World’s original purchase of Unifeeder was largely about getting wider exposure within the sector in its push to become a more integrated logistics provider. The Feedertech acquisition diversifies Unifeeder’s geographic and trade-lane exposure and as such, control of an Asian short-sea operator is arguably very helpful in DP World’s broader strategy of doing more end-to-end logistics in the Far East/ISC.”

Commenting on the competitive landscape was container analyst Alphaliner, which described the deal to create the soon-to-be unified ocean feeder /short-sea carrier as “a major feeder operator.” The analyst added that entity would challenge “the current leader X-Press Feeders Group.”

Alphaliner added that X-Press would retain leadership in terms of fleet size of over 107,000 TEU, or twenty-foot equivalent units. X-Press states that it operates more than 110 vessels (up to new Panamax) of which 40 are owned. It sails more than 100 routes and calls at over 200 ports in Asia, the Middle East, Europe, the Mediterranean, Africa and Latin America.

Richards of Maritime Strategies International also turned his mind to the competitive feeder/short-sea landscape following the Unifeeder/Feedertech tie-up.

“On a very general level, the consolidation between liner companies on the intra-Asia trade will allow for the deployment of larger vessels. However, in this specific case, Feedertech is merging with an intra-Europe specialist and there won’t be a separate set of networks to combine. The immediate implications for intra-Asia trades are therefore limited.”

However, Richards added, as consolidation increases then there could be an increase in pressure on smaller specialists, assuming that vessels continue to get bigger.

Dramatis personae

Feedertech calls at 19 ports on five services linking China, Taiwan, the Philippines, Malaysia, Thailand, India, Pakistan and the United Arab Emirates. Feedertech’s short-sea subsidiary, Perma Shipping Line, calls at 10 ports in the Middle East; 12 ports around India and neighbouring countries; and at 19 ports around Northeast Asia and Southeast Asia. The Feedertech Group (Feeertech and Perma Shipping combined) generates an annual revenue of $200 million and transports over 600,000 TEU each year.

DP World is already very well-known for being a major container terminal operator. It has more than 150 operations in over 50 countries, handling more than 71.4 million TEU a year. In addition, it is already a substantial short-sea/feeder operator through its various acquisitions.

DP World bought Unifeeder for 660 million Euros ($765.6 million) in August 2018. Unifeeder reported 510 million Euros of revenues in 2017. That latter figure was equivalent to $611.9 million as at the end of December 2017. Unifeeder, like Feedertech, splits its business into feeder and short sea services and it also splits business geographically. Unifeeder covers northeast Europe with about 50 feeder port calls in far west Russia, the Baltic states, the Scandinavian countries, the Benelux, the U.K. and Portugal. The company can then truck or rail containers into numerous destinations all through north, northeastern and northwestern Europe. Meanwhile, Unifeeder sister feeder company Unimed calls at about 53 ports around the Mediterranean and it also operates in the intra-Red Sea market.

At the time of the Unifeeder acquisition, Sultan Ahmed Bin Sulayem, group chairman and CEO, DP World, commented on the rationale for the purchase of the European feeder operator as being one that “supports our strategy to grow in complementary sectors, strengthen our product offering and play a wider role in the global supply chain as a trade enabler… The ever-growing deployment of ultra-large container vessels has made high-quality connectivity from hub terminals crucial for our customers.”

DP World is already the owner of P&O Ferries, which it bought in 2006. P&O Ferries runs passenger and freight carrying roll-on/roll-off vessels to and from the United Kingdom and continental Europe. P&O sister company P&O Ferrymasters offers a wide range of air, road and sea freight forwarding and trucking to many destinations throughout Europe.

Acquisition funding raised

Jump forward in time to late November 2019, and it appears that DP World was hungry for another feeder operator. It raised acquisition capital worth $2.3 billion by listing two conventional bonds totaling $800 million and two “Sukuks” (Islamically compliant financial certificates with a contractual promise to buy-back the certificate at a future date at a given value) totaling about $1.5 billion on the Nasdaq Dubai. To be Islamically compliant, Sukuk funds must be used to buy identifiable or tangible assets and the purchaser of the Sukuk takes partial ownership of the asset.

The funds that DP World raised were specifically generated to fund growth opportunities and, at the time of the listing, Sultan Bin Sulayem referred to the DP World’s strategy to become a “logistics solutions provider to end-cargo owners.”

DP World leads… but will anyone follow?

Although DP World has clearly decided that its future lies, at least in part, in end-to-end logistics, container analyst Richards of Maritime Strategies International thinks it is unlikely that competing terminal operators will follow the Arabian company’s lead.

He notes that it is normally ocean shipping companies that found or buy container terminal companies and not the other way around. However, although the deal is clearly significant, Richards was thoughtful on potential issues raised by the tie-up and by the likely (or not) impacts on the Asian short-sea/feeder trades.

“By and large, we don’t expect competing container terminal operators will necessarily follow suit and buy their own Intra-Asia specialists. It remains to be seen whether this will generate significant operational synergies. Indeed, these acquisitions have historically been the other way round, with liner companies expanding into port ownership. Captive cargo and guaranteed volumes are obviously a good thing for a port operator.

“But, at the same time, the ‘true’ feeder/transhipment cargoes, as opposed to the end-to-end cargos within the region, are generated by the needs of the major liner companies. Whether or not the larger carriers choose to hub at DP World terminals and generate work for feeder specialists at that terminal is out of Unifeeder’s control. Also, the advantage to a liner company of controlling its own terminal is fairly clear from the perspective of container handling costs, but aside from better visibility in terms of volumes, the flipside of a tie-up with a liner company is less obvious for a port operator as one side’s costs is the other’s revenues.”

Boris Johnson may have won a resounding victory in U.K. elections last week, but fears that the Conservative government might fail to reach a trade deal agreement with the European Union (EU) have not dissipated.

As reported in FreightWaves, once Parliament has ratified Johnson’s withdrawal agreement, the European Parliament is expected to give its consent in January before the U.K. leaves the EU at the end of next month. The two sides will then try to strike a free trade deal by the end of 2020.

However, as FreightWaves reported last week, that will be no easy task and a no-deal Brexit, which would be hugely disruptive to supply chains, remains a strong possibility.

Freight transport representatives were quick to call on the Johnson government to ratify the withdrawal agreement and push on with negotiating a free trade deal.

Richard Burnett, chief executive of the Road Haulage Association, said any Brexit agreement should ensure that there is “enough time to implement and transition to any new arrangements for customs, lorry access regulations and labor. This is essential to maintain the U.K.’s supply chains.”

Time to deliver for PM Johnson

Robert Keen, Director General of the British International Freight Association (BIFA), said members of his trade association expected the Johnson government to deliver on its Brexit and withdrawal agreement promises.

“For the last three years, freight forwarding and logistics companies have done all they can to prepare for Brexit in the face of huge uncertainties,” he added.

“The mantra of the new government has been ‘Get Brexit Done,’ but that will only have any real meaning for BIFA members if the actual details of our future relationship with the EU are clear.

“That means providing them with assurances that they won’t face another no deal cliff-edge next year, nor a messy and disorderly exit from the EU.”

Keen said avoiding a no-deal Brexit should be a priority.

“In regards to a future trade agreement with the EU, I would urge the new government to seek and commit to a workable adjustment period once the details are revealed about the changes our members might face in regards to the movement of freight across borders,” he added.

“Now is not the time for arbitrary negotiating deadlines.”

No-deal Brexit ‘may well happen’

However, Andy Cliff, managing director of freight and international logistics experts Straightforward Consultancy, told FreightWaves last week that EU-U.K. negotiations would not be easy and a no-deal Brexit remained a strong possibility. He said that trade negotiations must be concluded by the end of 2020 and, if they were not, Prime Minister Johnson could use his majority in Parliament to push through a no-deal Brexit.

“Many, including myself, feel that a free trade deal is highly unlikely, as the U.K. could then be used as a ‘back door’ into the EU allowing the U.K. to set more attractive import tariffs which they’re unable to do now whilst in the EU Customs Union for imported goods, thus starving the EU of revenue and also incentivizing companies to locate in the U.K. instead of the EU.

“When you consider this, a free trade deal has to be very unlikely, as the EU will do whatever is needed to protect the integrity of the single market, so a hard Brexit may well happen after all. So be prepared!”

The Freight Transport Association (FTA) called on the Johnson government to push its withdrawal agreement through Parliament with haste to remove any chance of a chaotic no-deal Brexit on Jan. 31.

Friction-free trade a priority

Pauline Bastidon, FTA’s Head of Global and European Policy, said priority should then focus on securing a future trading deal with the EU.

“What logistics and supply chain managers need above all is clarity over Brexit’s end game,” she said.

“While the short-term priority is to ensure that the U.K. leaves with a ratified withdrawal agreement, we need answers to the big questions about our future trading arrangements with Europe.”

Bastidon added that most of the crucial topics related to trade and transport had not even been discussed with the EU and time was short. “Entering these negotiations with a clear picture of what logistics needs will be critical to its success,” she added.

“Minimizing frictions, red tape and costs should be at the heart of the negotiations if U.K. PLC is to continue trading effectively.”

According to the FTA, the top priorities for the logistics sector in an end agreement were clear processes for imports and exports between the U.K. and Europe and finding agreement on the Northern Ireland border, including establishing how and where any customs will be made.

The FTA also called for clarity on the future status of EU nationals living and working in the U.K., given that British companies already had 53,000 truck driver vacancies.

The loss of the 343,000 EU nationals working in British logistics firms could see vehicle movements and the supply chain as a whole come to a standstill, warned the FTA. More FreightWaves and American Shipper articles by Mike

DB Digital Ventures, the venture capital arm of German train operator Deutsche Bahn, has announced an investment in Skyports, a U.K.-based drone technology startup that is taking the aerial route to transport people and cargo. DB Digital Ventures is a pan-global venture capital firm that invests predominantly in the mobility and logistics space, with a portfolio comprised of startups like what3words, Talixo and Teralytics.

Drone technology is a subset of the vertical take-off and landing (VTOL) aircraft segment, which has seen astronomical growth in recent years within the logistics realm, as moving cargo via air can further expedite last-mile delivery in the age of e-commerce.

The possibilities of drone delivery are endless; business models can be fashioned to suit market needs. For instance, drones can be deployed across nuclear markets which can support and sustain localised vendors. A fruit vendor in one part of a town can use drones to deliver fresh products to its customers’ doorsteps in a matter of minutes. In the U.S., hypermarket chains like Walmart can find drone deliveries a promising prospect as about 90% of Americans live within 10 miles of a Walmart store.

Heavy-haul drones can be used to deliver products over longer ranges, helping companies tap into hard-to-access markets – like the Australian hinterlands or landlocked African communities.

Functional across London, Los Angeles and Singapore, Skyports operates end-to-end drones that it states are very safe to fly, are operated by qualified remotely stationed pilots and with full regulatory approval across each of the cities. The startup currently transports medical products including pathology samples, blood and tissue products, and also is into e-commerce deliveries that concern mid- and last-mile deliveries.

Apart from pioneering drone deliveries, Skyports also has a stake in developing landing infrastructure for those drones, helping create a connected infrastructure network that enables seamless deployment of point-to-point drone services.

Last week, Skyports announced that it had raised its Series A financing, with DB Digital Ventures featuring amongst the investors. Along with Deutsche Bahn, airport operator Groupe ADP and venture capital firm Levitate Capital were also a part of the fundraising round.

“The new capital allows us to build teams in multiple locations – we have recently opened offices in Singapore and on the West Coast of the U.S. – and continue to secure prime vertiport locations in markets that we hope will be first movers for urban aerial mobility [UAM],” said Duncan Walker, the founder and CEO of Skyports in his statement. “We are also growing the team within our drone deliveries business where our technology is now market leading and we are focused on commercialisation.”

Walker expected market progress to increase over the next two years, as vehicle manufacturers and government authorities recognize the increasing consumer interest and concentrate on developing better drone aircraft at scale and in certifying them for commercial purposes.

“Our unique relationships with the majority of the leading OEMs [original equipment manufacturers] enables us to support them and be in the right place at the right time. Regulations are opening up for passenger and cargo flights and a number of players, both cities and vehicle manufacturers, are working hard to be first,” commented Walker.

For DB Digital Ventures, Skyports will serve as an opportunity to expand its reach within both mobility and logistics segments, as drones can double up as passenger aircraft if the need arises. “As an environmentally minded provider of mobility services and a leader in electromobility, Deutsche Bahn is the perfect partner for us, a company promoting the use of electric, zero-emissions aircraft,” said Walker.

Boris Johnson’s resounding win in British elections became official Friday morning. But for shippers making preparations for the U.K.’s departure from the European Union (EU), very little has changed.

As reported in FreightWaves, once Parliament has ratified Johnson’s withdrawal agreement, the European Parliament will give its consent in January before the U.K. leaves the EU at the end of next month. The two sides will then try to strike a free trade deal by the end of 2020.

However, as FreightWaves previously reported, that will be no easy task and a no-deal Brexit, which would be hugely disruptive to supply chains, is a strong possibility.

“Boris Johnson’s emphatic win will certainly allow him to get his Withdrawal Bill through Parliament and enable the U.K. to leave the EU on 31st January as planned,” U.K.-based Andy Cliff, managing director of freight and international logistics experts Straightforward Consultancy, told FreightWaves earlier Friday.

“The concerns which many have, as I have said previously, is that the most important stage, trade negotiations with the EU, kick in straight away, and if they don’t go well in that 11-month time frame, we could indeed face a so-called hard Brexit [no-deal Brexit], which Boris will have the authority to carry out by way of his commanding majority in Parliament.

“Many, including myself, feel that a free trade deal is highly unlikely, as the U.K. could then be used as a ‘back door’ into the EU, allowing the U.K. to set more attractive import tariffs which they’re unable to do now whilst in the EU Customs Union for imported goods, thus starving the EU of revenue and also incentivising companies to locate in the U.K. instead of the EU.

“When you consider this, a free trade deal has to be very unlikely, as the EU will do whatever is needed to protect the integrity of the single market, so a hard Brexit may well happen after all. So be prepared!”

In an exclusive interview last week ahead of the election, Cliff explained to FreightWaves’ Mike King how shippers should best prepare for the many potential Brexit outcomes. The full interview follows:

FW: Brexit was delayed again at the end of October until Jan. 31. But for shippers, has anything practically changed in how they organize shipments between the U.K. and the rest of the world since the original referendum in 2016?

Cliff: It’s a good question, Mike, and many companies based in the U.S. are thinking quite justifiably that something must have changed, especially with the amount of time that’s passed and the extensive negotiations that have been taking place ahead of the U.K.’s departure from the EU.

However, nothing has changed both in terms of logistics and Customs procedures for U.K. importers and exporters, and they won’t change until we [the U.K.] either leave the EU with a deal or we opt for a so-called “hard Brexit,” where the U.K. then becomes a third country and defaults to World Trade Organization (WTO) rules.

If we do leave with a deal, a transitionary period of 12 months will kick in where everything stays the same, and talks over the actual trading relationship will begin, although that transition period will most likely need to be extended given the size of the task!

FW: So, the big focus for shippers throughout this more than three-year process has been about how to prepare for a highly disruptive ‘hard’ or no-deal Brexit, and that is still possible Jan. 31?

Cliff: Absolutely, Mike, and this is why the U.K. Parliament became logjammed in November — which then brought about the general election set for Dec. 12. We have had many discussions with U.K. companies [some with U.S. operations] on making sure that not only they are prepared, but that their freight providers are ready too, because in a hard-Brexit scenario, we will see the return of Customs borders between the U.K. and EU, and this will then require Customs declarations on both sides and all it entails.

When you break it down, there are three key areas to consider: Are you ready, is your freight forwarder ready, and just as important, have you engaged with your EU customers to explain how their delivery times will be impacted, and to agree who will bear extra costs such as Customs duties.

Also, Incoterms will now come into sharp focus in this market, as in the past U.K. companies would often sell or buy on a “delivered price” and Incoterms were either vague or not even quoted in contracts. In October we compiled a Brexit checklist to assist U.K. companies with hard-Brexit preparations that is written in plain language and covers guidance for both U.K. importers and exporters that has been well-received.

FW: Previously FreightWaves has explored how and why Brexit will reshape Europe’s logistics landscape in the medium and long term. But more immediately, what does a no-deal Brexit mean for shippers outside of the EU — for example, in the U.S.?

Cliff: Well, Mike, as I said earlier, many U.S. companies have a European headquarters in the U.K. that will then distribute their products around the whole of Europe. So if they currently operate in this way, then they will be affected. They will need to understand that delays in delivery or extra costs from the U.K. to the EU may need to be communicated to manufacturing and sales so they manufacture or ship earlier and potentially review their export pricing to help their U.K. operation retain margin.

FW: What should shippers in the U.S. be doing to prepare for a no-deal Brexit?

Cliff: They need to be talking to their U.K. sites to satisfy themselves that their U.K. operation is prepared and their EU customers are clear on the terms and costs of future purchases, and also, most importantly, delivery times. This is an area we have come across several times, where the front-line shipping/logistics operation in the U.K. tells their senior management that they’re ready, but when you conduct an analysis of the basics, they just aren’t ready, and they haven’t covered all the bases I referred to earlier.

FW: What is the state of preparedness of U.K. shippers and their EU counterparts in your view?

Cliff: To be honest, based on the companies we’ve talked with and met, we’ve been pretty concerned, as they really haven’t found out enough from their freight forwarders about how the service they currently receive will change, both in cost or transit time, and there’s been little engagement with end-customers to communicate how they will continue to supply them, and at what cost and time frame.

From the EU side, where a U.K. company is buying product from, say, Germany, these EU suppliers have come to the party quite late and you get the distinct impression that they are also getting vague assurances from their EU-based freight providers on how they will operate in a hard-Brexit scenario.

So, overall, we are very concerned about the state of readiness of both the logistics providers and U.K. exporters in particular. In the U.K., however, we do have special measures set in place by U.K. Customs to help U.K. importers through a hard Brexit — so- called “Transitional Simplified Procedures” — but again, many companies have not applied for these procedures or, even if they have, they haven’t had the necessary dialogue with their freight forwarders to make it work from Day One.

FW: What can U.K. or EU shippers do now to prepare better for a no-deal Brexit?

Well, they really need to carry out an urgent review of the three areas I mentioned earlier, and only then will they know where the gaps are. Based on the dialogue we’ve had with freight forwarders, although they may have issued customer Brexit bulletins, they’re often overloaded with industry jargon and incomplete. We also don’t feel they’ve considered the whole sales transaction (from shipper dispatch to final customer delivery) and everything that will be affected as a result. For example, if you decide you will sell on Incoterms DAP, where the U.K. exporter pays for all freight costs to the door, excluding duties and brokerage, has your freight forwarder had any dialogue with your EU customer to set up Customs brokerage procedures and credit arrangements for costs of Customs entry, duties and taxes to ensure continuity of service? It’s unlikely.

FW: Aside from a no-deal Brexit, Boris Johnson’s government had already agreed to a deal with the EU. If after the general election that becomes law, what are the key takeaways of that deal that shippers should be aware of?

If Boris Johnson’s Conservative government wins the election on Dec. 12 with a clear majority, he should be able to get this new deal through Parliament, and then we enter the transitionary period, where everything remains as it is now.

It’s worth saying again, however, that many think the December 2020 time frame is way too short to secure a U.K./EU trade deal, and if the U.K. had left with a deal on the original leave date of March 29, we would then have had 21 months to get this over the line.

If we assume that Boris Johnson wins on December 12 with a clear majority, he will push his withdrawal agreement through Parliament and we will leave on Jan. 31, and the transition period kicks in along with the start of trade deal negotiations. The concern many have is that if the EU won’t play ball and give the U.K. a “free trade deal” akin to what we have today, he may then take us out with a hard Brexit on Dec. 31, 2020, or potentially even before that if things are going badly.

So, in our opinion, the best approach is to prepare for a hard Brexit and avoid placing your supply chain and business at risk. It’s the only way to be sure. Then you can sleep at night!

Andy Cliff, managing director of freight and international logistics experts, Straightforward Consultancy.

The U.K.’s departure from the European Union (EU) moved a decisive step closer in the early hours of Friday morning when the Conservative Party headed by Boris Johnson won a decisive general election victory.

In the buildup to the election, Johnson had consistently promised to “Get Brexit Done.” And, after winning a huge parliamentary majority of at least 78 seats — 364 out of 650 seats, with one still to declare at this writing — he doubled down on his pledge, vowing to push his EU withdrawal agreement through Parliament in time for Brexit on Jan. 31.

“We politicians have squandered the last three-and-a-half years in squabbles about Brexit. We have even been arguing about arguing, about the tone of our arguments,” he said. “I will put an end to all that nonsense, and we will get Brexit done on time by the 31 January.

“No ifs, no buts, no maybes — leaving the European Union as one United Kingdom, taking back control of our laws, borders, money, our trade, immigration system, delivering on the democratic mandate of the people.”

Once Parliament has ratified Johnson’s withdrawal agreement, the European Parliament will give its consent in January before the UK’s departure from the EU at the end of next month. The two sides will then try to strike a free trade deal by the end of 2020, although as FreightWaves has previously reported, that will be no easy task. A no-deal Brexit, which would be hugely disruptive to supply chains, remains a strong possibility.

“We expect as soon as possible a vote by the British Parliament on the withdrawal agreement,” said Charles Michel, the European Council president. “It is important to have the clarity as soon as possible. We are ready. The EU will negotiate to ensure to have a close cooperation in the future with the U.K.”

The FTSE and sterling surged on Johnson’s victory, while opposition leader Jeremy Corbyn, whose Labour Party won just 203 seats, hinted he would step down once a new leader was elected.

President Donald Trump urged Johnson to “celebrate” and then prepare to sign a major new trans-Atlantic trade deal with the U.S.

He tweeted: “Congratulations to Boris Johnson on his great WIN! Britain and the United States will now be free to strike a massive new Trade Deal after BREXIT.”

GIC, Singapore’s sovereign wealth fund, has announced the acquisition of a Pan-European logistics real estate portfolio from Apollo Global Management, a private-equity firm, to the tune of €950 million. This is one of the largest investments made in the European real estate segment this year and shows the interest of GIC to consolidate its presence in the ever-expanding European logistics market.

The acquisition will be via GIC’s P3 Logistic Parks, its fully owned logistics platform, which the wealth fund looks to push for dominion in the European logistics property space. Apollo’s portfolio, termed “Maximus,” is comprised of 28 logistics assets that are spread across core logistics hubs in Austria, Belgium, Germany, Poland, the Netherlands and Slovakia.

The Maximus portfolio covers more than 1 million square meters of industrial space, which will now be controlled by P3 in its attempt to improve its market standing in Europe. GIC bought P3 in 2016 for €2.4 billion to diversify its income-producing portfolio and increase its real estate scope within the continent.

“The portfolio’s well-diversified tenant base includes companies in the automotive, e-mobility, distribution, e-commerce and last-mile logistics sectors, among others. The acquisition is expected to close during the first quarter of 2020, subject to customary closing conditions and any requisite regulatory approvals,” said GIC in its statement.

The European logistics real estate market is regularly witnessing high-value deals go through. For example, Dutch logistics service provider Vos Logistics acquired SNEL Shared Logistics last week, getting control of a 65,000-square-meter warehouse in Woerden, the Netherlands. This acquisition is expected to help Vos Logistics offer logistics services across four major cities in the Netherlands — Amsterdam, Rotterdam, Den Hague and Utrecht.

“As a long-term value investor, logistics continues to be an attractive sector for GIC,” said Lee Kok Sun, the chief investment officer at GIC Real Estate. “It is set to keep growing, supported by strong e-commerce growth, and we expect it to generate steady income streams in the long run.”

Headquartered in Prague, Czech Republic, P3 owns and operates properties across 13 countries that have more than 5.3 million square meters in assets.

Otis Spencer, the chief investment officer of P3, expressed confidence with integrating the Maximus portfolio within the company’s platform, explaining that it will equip P3 with a team and resources that will help them successfully manage and add value to the assets and the end customer.

“This [acquisition] reflects our multifaceted investment strategy to grow our market share in the Pan-European market through both development and acquisition. With the support of our owner, GIC, we are actively looking for further investment deals to strengthen our position as one of Europe’s leading developers and managers of logistics properties,” said Spencer.

A Christmas season strike by truckers hauling merchandise for retail giant Argos, which operates in the U.K. and Ireland, has been called off. Yard and highway drivers employed by UPS at Argos’ flagship distribution center at Barton in Staffordshire, England, secured a pay hike deal worth about 4.5%, according to a Dec. 12 announcement from trade union Unite.

More than 40 Unite members, representing 90% of workers who maneuver loads around the distribution center, voted in favor of the pay deal from UPS management, following talks with arbitration service Acas.

Work will continue over the holiday period at the distribution center, with back pay and the agreed increase set to be paid before Christmas.

Workers warned of a 15-day strike following a 10-month wage dispute if a deal could not be reached. The strike was set to start late Dec. 17 and continue through year’s end.

The union warned that the proposed job action would effectively grind operations to a halt, causing severe disruption to Argos at its busiest time of the year.

Argos is a major player in the retail sector with more than 883 retail shops, 29 million shop customers yearly and nearly 1 billion online visitors annually. The Barton site is a critical hub in Argos’ national network and the location from which all high-end electrical items, including smartphones, laptops and televisions, are shipped to regional Argos distribution centers for delivery to stores.

With high-sulfur fuels currently around half the price of low-sulfur options, container lines are rushing vessels to shipyards to get scrubbers fitted ahead of new International Maritime Organization (IMO) rules that become mandatory at the start of 2020.

The rules state that unless some form of emission abatement technology such as scrubbers has been installed on vessels, the sulfur content of fuel oil burned by ships operating outside designated emission control areas must not exceed 0.5%, compared to 3.5% now.

According to Alphaliner, more than 10% of container ship capacity will be fitted with scrubbers by January, with more to follow over the next two years. The differential between high-sulfur fuel (HFO) and low-sulfur fuel (LSFO) prices is the main driver of scrubber demand.

“The very high take-up rate for scrubbers reflects the attractive economics for these ships with the current price spread for low-sulfur fuel oil over HFO already reaching $250 per ton, which would provide the operators of these ships with substantial savings compared to conventional units that would need to switch to LSFO,” said a note from Alphaliner.

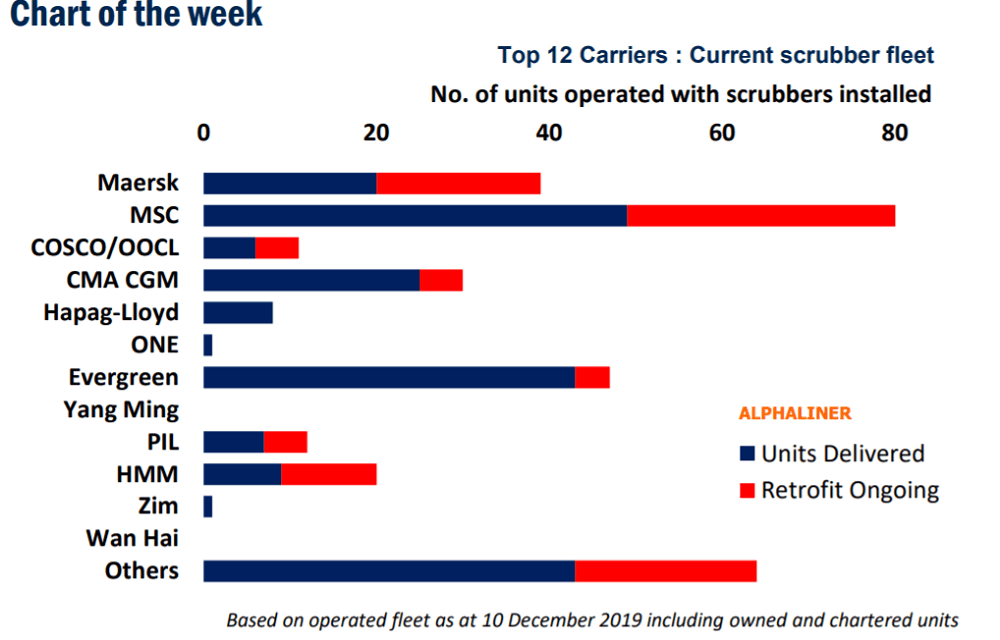

However, the strategy of carriers is widely divergent (see chart below), with some including Mediterranean Shipping Company (MSC) and Maersk betting big on scrubbers, while others including Ocean Network Express (ONE) are hoping that low-sulfur prices will eventually subside.

Source: Alphaliner

A rising scrubber tide

The attraction of scrubbers has gradually increased through 2019 (see chart below). The number of container ships fitted with sulfur scrubbers reached 212 units (1.79 million twenty-foot equivalent units or TEUs) on Dec. 10, according to Alphaliner, with an additional 101 units currently at repair yards undergoing retrofits.

“Taken together, the scrubber-fitted ships will account for some 5.9% of the total number of container ships — or 11.8% of the total TEU capacity of the global fleet — by early 2020 when the new IMO 2020 sulfur cap comes into effect,” said Alphaliner.

“More scrubber-fitted container ships are expected to be delivered in the next two years, including both newbuildings and retrofitted units that could possibly bring their total number to some 1,000 ships for 10 million TEU by the end of 2022.”

Source: Alphaliner

The cost to lines of yard delays

However, the long line of container ships waiting to enter repair yards and their extended stays while there being fitted with scrubbers is costing carriers dearly in terms of vessel downtime, noted Alphaliner.

Average yard stays for vessels undergoing retrofits is now around 59 days, with 17% of vessels now out of action for more than 80 days. For larger ships, the cost of the downtime could be as much as $30,000 to $50,000 per day, although as FreightWaves has reported, the reduction in capacity is helping support spot freight rates.

“MSC has been the most badly affected by these delays, with at least 15 of its ships clocking yard stays of over 80 days” reported Alphaliner. “The yard delays are also causing severe congestion with at least five MSC ships currently waiting for up to eight weeks to enter the repair yards, with shipyards in the Zhoushan region in China especially congested in the last two months.”

However, those carriers that take the pain of lost revenues now are set to gain next year from lower operating costs.

“These ships will be able to enjoy the lower price of standard heavy fuel oil, with current IFO380 bunker price dropping to just $255/ton compared to LSFO price of over $510/ton [based on prices at Rotterdam],” noted Alphaliner.

More FreightWaves and American Shipper articles by Mike

The International Air Transport Association (IATA) broke out in seasonal goodwill on Dec. 11, predicting that a new year will bring fresh cheer for the cargo sector.

Cargo traffic is expected to grow 2.0% in 2020 after a year of slowing economic growth, trade wars, geopolitical tensions, uncertainty over Brexit and social unrest contributed to a 3.3% contraction in airline freight business, Director General Alexandre de Juniac said in an annual address to media at the group’s Swiss headquarters.

It was the first downturn for the sector in seven years. The 3.3% annual decline in demand was the steepest drop since 2009, during the global financial crisis.

IATA is forecasting 62.4 million cargo tons in 2020, a 2% increase over the 61.2 million tons carried in 2019, as world trade rebounds. The 2019 tally represents the lowest aggregate tonnage figure in three years. The IATA forecast values international trade shipped by air next year at $7.1 trillion.

Yields will continue to slide, with a 3% decline forecast for 2020, an improvement from a 5% decline in 2019. Cargo revenues will slip for a third year in 2020, with revenues expected to total $101.2 billion, down 1.1% from 2019, according to IATA.

The worldwide freight load factor, measured as a percentage of available freight ton kilometers (AFTKs), is forecast at 46.3%, down slightly from 46.7% estimated for the current year and 49.3% posted for 2018.

IATA estimates the global airline industry will produce a net profit of $29.3 billion in 2020, up from $25.9 billion expected in 2019 (revised downward from $28 billion forecast in June.) Achieving that would make 2020 the industry’s 11th consecutive year in the black.

Airlines in Asia Pacific were the most exposed to weakness in world trade and cargo this year. The modest recovery in world trade will support profits next year in the region, according to the forecast.

2019 was a difficult business environment for airlines, “yet the industry managed to achieve a decade in the black, as restructuring and cost-cutting continued to pay dividends. It appears that 2019 will be the bottom of the current economic cycle, and the forecast for 2020 is somewhat brighter,” de Juniac said.

IATA and the World Bank anticipate global GDP to expand by 2.7% in 2020 (marginally above the 2.5% growth in 2019). World trade growth is expected to rebound to 3.3% from 0.9% in 2019, with easing of some trade tensions expected.

IATA reported in October that airline CFOs and heads of cargo were positive about future growth in air travel but less positive about cargo due to the slowdown in world trade as a result of trade disputes. However, central banks have reacted to the slowdown by easing monetary policy, and governments have used fiscal policy to stimulate domestic demand, limiting the risk of recession.

The regional profit picture is mixed in both 2019 and 2020. Africa, the Middle East and Latin America are all expected to lose money in 2019, with carriers in Latin America returning to profit in 2020 as regional economies strengthen. Airlines in North America continue to lead on financial performance, accounting for 65% of industry profits in 2019 and around 56% of aggregate earnings in 2020. Financial performance is expected to improve or remain the same compared to 2019 in all regions except for North America, where expected capacity growth owing to new aircraft deliveries could put pressure on earnings, according to IATA.